TL;DR:

- Rideshare accident laws determine which insurance policy applies based on the driver’s app status during a crash. Knowing the active coverage period is crucial for maximizing compensation and involves documenting app activity and incident details promptly. Liability depends on negligent driving, company responsibility, or third-party involvement, with legal strategies varying by state.

Rideshare accident laws are the legal rules that determine who pays for injuries and damages when a crash involves an Uber or Lyft driver, and which insurance policy applies depends entirely on what the driver was doing at the moment of impact. These laws sit at the intersection of personal injury law, insurance contract law, and transportation network company (TNC) regulations. Unlike a standard car accident, a rideshare crash can involve your own insurer, the driver’s personal policy, and a TNC commercial policy all at once. Knowing how these layers interact is the first step toward protecting your right to full compensation.

How rideshare accident laws define coverage by driver app status

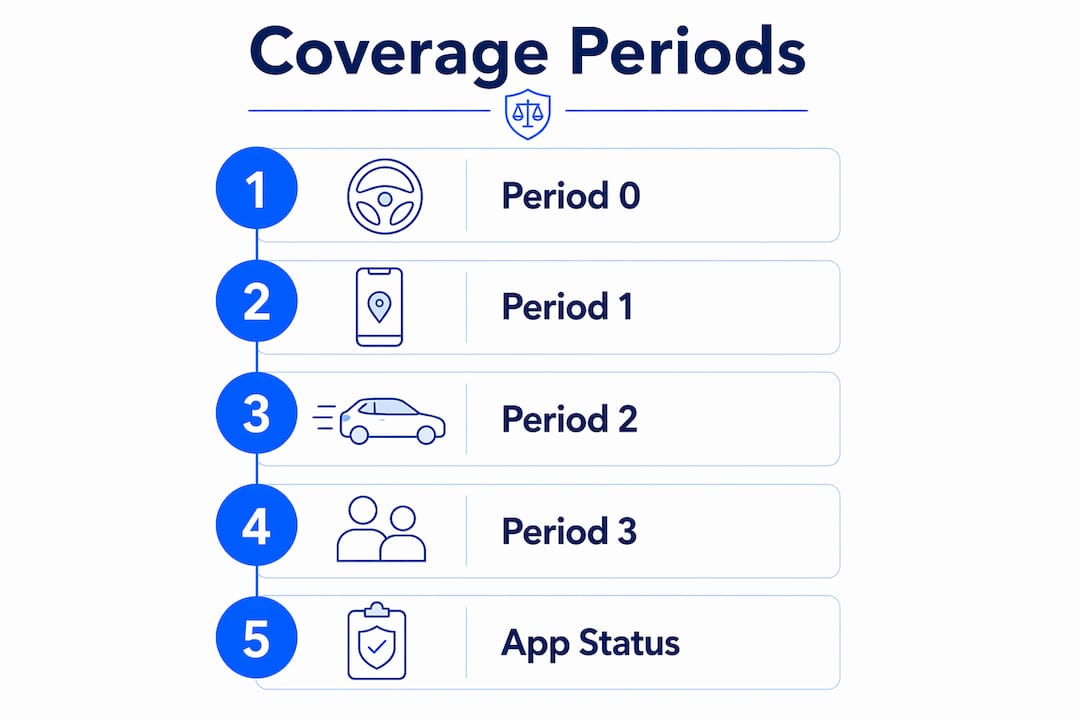

The single most important factor in any rideshare injury claim is the driver’s app status at the time of the crash. App status determines whether primary, secondary, or contingent coverage applies, and which insurer you must pursue first. Most states recognize four distinct periods.

| Coverage Period | Driver Status | Insurance That Applies |

|---|---|---|

| Period 0 (app off) | Personal driving, no TNC activity | Driver’s personal auto policy only |

| Period 1 (app on, no ride accepted) | Logged in, waiting for a request | Contingent TNC liability coverage |

| Period 2 (ride accepted, en route) | Driving to pick up a passenger | TNC primary commercial coverage |

| Period 3 (passenger onboard) | Active trip in progress | TNC primary commercial coverage |

In California, a well-documented example, Period 1 offers $50K/$100K in contingent liability, while Periods 2 and 3 carry $1 million in primary liability coverage. That gap between $100,000 and $1 million is enormous for a seriously injured victim, and it all hinges on a timestamp in the app.

When the app is off, only the driver’s personal policy applies. The problem is that standard personal auto insurance frequently excludes commercial rideshare use, which can leave victims with no viable coverage to pursue. This is the most dangerous gap in the entire rideshare insurance system.

Pro Tip: Screenshot the ride details in your Uber or Lyft app immediately after any crash. That record shows the trip status, driver name, and timestamp. It is some of the most valuable evidence your attorney will use to establish which coverage period was active.

App GPS tracking and ride logs are the primary tools used in litigation to confirm the coverage period. If that data is lost or disputed, your claim becomes significantly harder to prove.

Who is legally liable after a rideshare crash?

Liability in a rideshare accident follows standard negligence law: the injured party must show the driver owed a duty of care, breached it, and caused the resulting harm. What makes rideshare cases more complex is the question of whether the TNC company itself shares responsibility.

Whether you can sue the rideshare company depends on whether the driver is classified as an employee or an independent contractor. In most states, Uber and Lyft classify their drivers as independent contractors, which shields the companies from direct vicarious liability. That classification is not always airtight, however. Courts in several states have challenged it, and state-specific labor laws can shift that analysis significantly.

Potential liable parties in a rideshare accident include:

- The rideshare driver, for negligent operation including distracted driving, fatigue, or traffic violations

- The TNC company, in cases of negligent hiring, inadequate background checks, or known safety failures

- A third-party driver, if another vehicle caused or contributed to the crash

- A vehicle manufacturer, if a defect contributed to the collision

Evidence of driver negligence often includes cell phone records, event data recorder (EDR) output, and app activity logs. These sources can establish whether the driver was distracted by the app itself at the moment of impact, which creates a direct line of liability back to the platform’s design and notification system.

Third-party liability adds another layer. If another driver caused the crash, you may have claims against that driver’s insurer and the TNC’s underinsured motorist coverage simultaneously. Coordinating those claims without legal help is where most victims lose money.

What to do after a rideshare accident to protect your claim

The actions you take in the first 24 to 48 hours after a rideshare crash directly affect the strength of your claim. Follow these steps without exception.

- Call 911 immediately. A police report creates an official record of the crash, the parties involved, and initial fault observations. Never skip this step, even for crashes that appear minor.

- Document the driver’s information. Collect the driver’s name, license plate, and insurance details. Take a screenshot of the active ride in the Uber or Lyft app before closing it.

- Photograph everything. Capture vehicle damage, road conditions, traffic signals, skid marks, and any visible injuries. Time-stamped photos are admissible evidence.

- Seek medical attention the same day. Even if you feel fine, some injuries like whiplash or internal trauma do not present symptoms immediately. A same-day medical record ties your injuries directly to the crash.

- Report the crash to the TNC. Both Uber and Lyft have in-app accident reporting tools. File a report to create an official record with the company.

- Notify your own insurer. In no-fault insurance states, you are required to file with your own carrier first before pursuing other parties. Failing to notify your insurer promptly can result in a claim denial.

- Consult a personal injury attorney before giving statements. Insurance adjusters from any party will contact you quickly. Do not provide recorded statements without legal counsel.

Pro Tip: Do not post about the accident on social media. Insurance companies and defense attorneys routinely monitor claimants’ social media accounts, and a single photo or comment can be used to minimize your injuries or undermine your credibility.

Understanding your rideshare accident legal rights before speaking to any insurer gives you a real advantage. Most victims who settle quickly leave significant money on the table.

How rideshare accident compensation is calculated

Compensation in a rideshare injury claim covers both economic and non-economic damages. The total value of your claim depends on the severity of your injuries, the applicable insurance coverage period, and the skill of your legal representation.

Compensable damages typically include:

- Medical expenses: Emergency care, surgery, hospitalization, physical therapy, and future treatment costs

- Lost wages: Income lost during recovery, plus reduced earning capacity if the injury is permanent

- Pain and suffering: Physical pain, emotional distress, and reduced quality of life

- Property damage: Repair or replacement of your vehicle or personal property

The coverage period at the time of the crash sets the ceiling on available insurance funds. A Period 1 crash in California, for example, caps contingent liability at $100,000 per person. A Period 3 crash opens up $1 million in TNC primary coverage. That difference can be the gap between a fair settlement and financial hardship.

One significant change affects California claims filed after October 1, 2025. Under SB 371 and AB 1340, uninsured and underinsured motorist (UM/UIM) coverage for rideshare companies dropped from $1 million to $60,000 per person. This reduction means victims hit by uninsured drivers during active Uber or Lyft trips face a dramatically lower safety net than they did before. Victims in other states should check their state’s TNC insurance statutes for similar legislative changes.

Early legal advice consistently produces higher settlements. Attorneys who specialize in rideshare claims know how to stack coverage sources, challenge independent contractor classifications, and counter lowball offers from TNC insurance adjusters. Handling these claims alone, against experienced insurance defense teams, rarely produces the best outcome.

Key takeaways

Rideshare accident compensation depends on the driver’s app status at the time of the crash, which determines the applicable insurance policy and the maximum coverage available to injured parties.

| Point | Details |

|---|---|

| App status controls coverage | The driver’s period (0 through 3) determines which insurer pays and how much coverage applies. |

| Independent contractor status limits TNC liability | Most rideshare companies avoid direct liability by classifying drivers as contractors, not employees. |

| Act fast to preserve evidence | App screenshots, police reports, and same-day medical records are the foundation of a strong claim. |

| Coverage gaps are real and costly | Period 1 crashes often expose victims to far lower limits than Period 2 or 3 crashes. |

| Legal representation increases recovery | Attorneys who know TNC insurance rules consistently secure higher settlements than self-represented claimants. |

What I’ve learned from watching rideshare claims go wrong

The most common mistake I see victims make is assuming the rideshare company’s insurer is on their side. It is not. Uber and Lyft’s insurance carriers are sophisticated operations with one goal: minimize payouts. When a victim calls without legal representation, they are negotiating against professionals who handle hundreds of these claims every month.

The app status issue is where I see the most damage done. Victims often do not know what period the driver was in, and by the time they try to find out, the data is harder to access. Coverage gaps during Period 1 are particularly brutal because the contingent coverage only activates if the driver’s personal policy denies the claim first. That process takes time, and victims are left waiting while bills pile up.

State law matters more than most people realize. Georgia, where Jewkesfirm operates, follows a tort-based system rather than no-fault, which means you can pursue the at-fault driver directly without first filing with your own insurer. That changes the strategy entirely compared to a state like Florida or Michigan. Knowing your state’s rules before you make any moves is not optional. It is the difference between a well-timed claim and a procedural mistake that costs you thousands.

My honest advice: review your own auto insurance policy before your next rideshare trip. Check whether you carry UM/UIM coverage and at what limits. If you are ever in a crash during a Period 1 trip, that coverage may be the only meaningful protection you have.

— Ali

Injured in a rideshare crash? Jewkesfirm can help

If you were hurt in an Uber or Lyft accident in South Atlanta or the surrounding Georgia counties, Jewkesfirm is ready to fight for the compensation you deserve. The firm’s attorneys understand TNC insurance structures, app status disputes, and the tactics insurers use to minimize rideshare injury claims. Jewkesfirm handles cases on a contingency fee basis, meaning you pay nothing unless they win. Learn more about what a rideshare claim involves or contact the firm today for a FREE CONSULTATION to get your case reviewed by an experienced personal injury attorney.

FAQ

What are rideshare accident laws?

Rideshare accident laws are the legal rules governing liability and insurance coverage when a crash involves a TNC driver such as Uber or Lyft. They determine which policy applies based on the driver’s app status at the time of the crash.

Who pays for injuries in a rideshare accident?

The responsible insurer depends on the driver’s app status. Period 2 and 3 crashes trigger the TNC’s $1 million primary commercial policy, while Period 0 crashes fall to the driver’s personal insurer only.

Can I sue Uber or Lyft directly after an accident?

In most states, rideshare drivers are classified as independent contractors, which limits direct liability against the company. Exceptions exist when the company was negligent in hiring or retaining the driver.

What if the rideshare driver had no valid insurance?

If the driver’s personal policy excludes rideshare use and the app was off, you may face a coverage gap. Your own UM/UIM coverage becomes critical in this scenario, which is why personal injury checklists recommend reviewing your own policy limits before any rideshare trip.

How long do I have to file a rideshare injury claim in Georgia?

Georgia’s statute of limitations for personal injury claims is generally two years from the date of the accident. Missing this deadline eliminates your right to compensation, so consulting an attorney as soon as possible after the crash is the safest course of action.