TL;DR:

- Most truck accident victims face insurance layers that fall short of covering their full damages, especially with outdated minimum liability requirements.

- Understanding multiple insurance policies, insurer tactics, and the importance of legal counsel is essential to maximize compensation after a crash.

Most people assume that because commercial trucks are required to carry insurance, they’ll be fully covered after a crash. That assumption can cost you. The role of insurance in truck crashes is far more complex than a single policy payout, and the gap between what insurers are legally required to carry and what a catastrophic injury actually costs can be staggering. If you’ve been hurt in a truck accident in Georgia, understanding how trucking insurance really works, including the layers, the limits, and the tactics, is the first step toward protecting your rights and your financial recovery.

Table of Contents

- Key takeaways

- The role of insurance in truck crashes: why minimums fall short

- How trucking insurance coverage actually works

- What insurance companies do after a truck crash

- Strategies for maximizing your compensation

- Current coverage limits vs. what victims actually need

- My perspective on insurance and truck crash victims

- How Jewkesfirm helps truck accident victims fight back

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Federal minimums are outdated | The $750,000 federal minimum has not kept pace with inflation or rising medical costs, leaving many victims undercompensated. |

| Multiple insurance layers exist | Trucking companies often carry excess and umbrella policies above the minimum that victims may be entitled to pursue. |

| Insurers use aggressive tactics | Expect insurers to dispute evidence, delay access to records, and offer low settlements quickly after a crash. |

| Proposed legislation could help | The 2026 Fair Compensation for Truck Crash Victims Act would raise minimums to $5 million, indexed to inflation. |

| Legal counsel is critical | An attorney experienced in trucking claims can identify all applicable policies and protect your right to full compensation. |

The role of insurance in truck crashes: why minimums fall short

When a commercial truck injures someone on the road, the financial recovery process runs through the world of commercial auto liability insurance, the industry term for the primary coverage trucking companies are required to carry. Most people hear “insurance” and think it means they’ll be taken care of. The reality is more complicated.

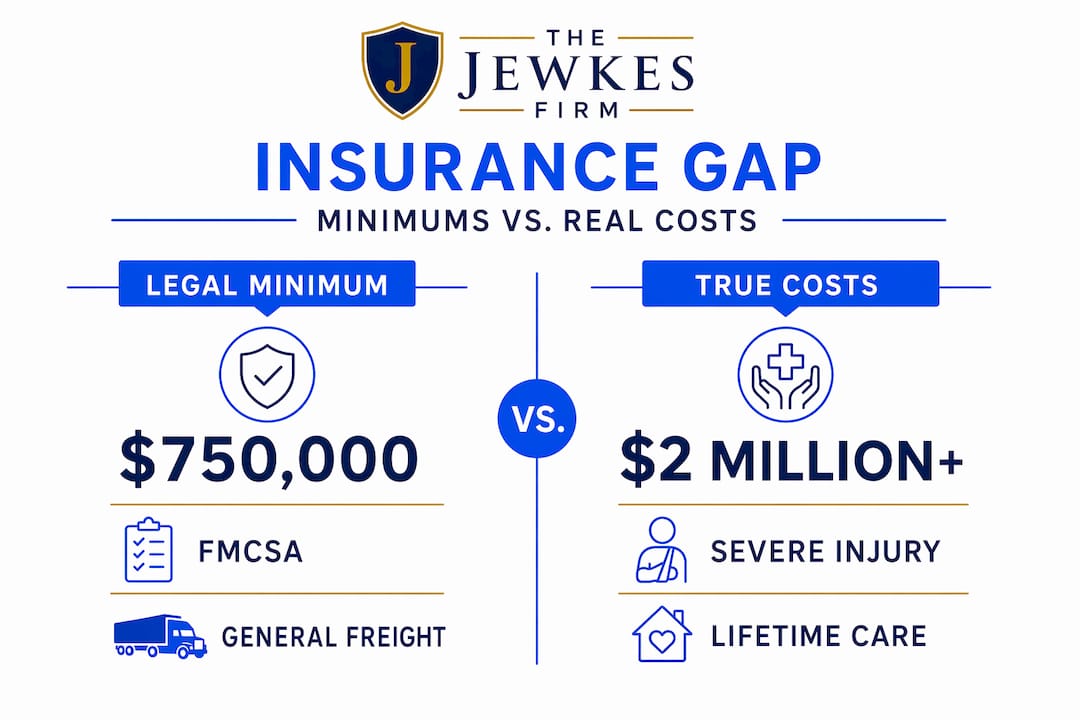

The Federal Motor Carrier Safety Administration (FMCSA) requires minimum liability of $750,000 for most interstate general freight carriers. Trucks hauling hazardous materials can carry requirements as high as $5,000,000, while some smaller vehicles are required to carry only $300,000. These numbers sound substantial until you price out a catastrophic injury.

Severe truck accident injuries, including spinal cord damage, traumatic brain injuries, and amputations, routinely generate medical bills that exceed $1 million when you factor in emergency care, surgery, rehabilitation, and long-term support. Economists and safety researchers have calculated that adjusted for inflation and modern medical costs, the $750,000 minimum would need to be somewhere between $2.2 million and $3.7 million to hold the same real-world value it was intended to carry when first established.

| Coverage Type | Federal Minimum | Inflation-Adjusted Value |

|---|---|---|

| General freight (interstate) | $750,000 | $2.2M to $3.7M |

| Hazardous materials (highway) | $5,000,000 | Up to date |

| Oil transport | $1,000,000 | Moderately outdated |

| Smaller commercial trucks | $300,000 | Severely outdated |

Pro Tip: Never assume the minimum coverage limit is the only money available to you. Many trucking companies carry excess policies well above federal minimums, and identifying those layers early in your claim matters.

How trucking insurance coverage actually works

Understanding how coverage layers stack is where most truck accident victims get lost. Primary commercial auto liability is the foundation. It covers bodily injury and property damage caused by the truck driver’s negligence. But that’s rarely the only policy in play.

Most large trucking companies carry excess or umbrella liability policies that sit above the primary coverage. These kick in once the primary policy limit is exhausted. For a catastrophic crash, this distinction between primary and excess coverage is the difference between a partial recovery and a full one. Catastrophic damages frequently exceed primary policy limits, which means victims and their attorneys must identify and pursue multiple insurers at once.

Here’s what the full insurance picture in a truck crash typically looks like:

- Primary commercial auto liability: Covers the trucking company and driver for bodily injury and property damage up to the policy limit

- Excess or umbrella liability: Provides additional coverage above the primary limit, often held by large carriers with significant assets

- Cargo insurance: Covers damage to freight, not passengers, but relevant in multi-vehicle pileups

- Occupational accident or workers’ comp: May apply to the driver, not the victim, but affects how fault is allocated

- Employer’s non-owned auto coverage: Relevant when independent contractors are involved

The claims process for truck collisions moves through these layers sequentially. If you settle too early with the primary insurer and sign a release, you may forfeit your right to pursue excess coverage.

Pro Tip: Never accept a settlement offer from any insurer without first confirming that all applicable policy layers have been identified. An experienced trucking attorney can pull insurance certificates and coverage declarations that you wouldn’t know to request on your own.

What insurance companies do after a truck crash

Here’s something most victims don’t realize until it’s too late. Insurance companies focus on defending their policyholders, and their goal after a crash is to limit what they pay out, not to help you recover. That’s not cynicism. That’s how the business works.

The tactics are well-documented and consistent:

- Disputing liability: Shifting blame to the victim, road conditions, or a third party to reduce the insurer’s exposure

- Withholding evidence: Delaying access to driver logs, black box data, and surveillance footage that could establish fault

- Fast, low settlement offers: Reaching out quickly while you’re still in shock to secure a release before you understand the full scope of your damages

- Surveillance and social media monitoring: Using your own posts and photos as evidence that your injuries are less severe than claimed

“The insurance company’s adjuster is not your advocate. They are trained professionals working to protect their employer’s bottom line. Treating their first offer as a starting point, not a final answer, is one of the most important things a crash victim can do.”

There’s also a broader industry dynamic worth understanding. Commercial auto liability costs increased 18.6% from 2021 to 2024, even as crash rates declined. Liability losses per mile rose by 33.1%, driven largely by claim expenses and litigation costs. Insurers use this “social inflation” narrative to justify aggressive claim defense, which directly affects how they handle your case.

Strategies for maximizing your compensation

Knowing that insurance companies will resist your claim is only useful if you respond strategically. Here’s what actually makes a difference in truck accident insurance claims:

-

Identify every responsible party. The driver, the trucking company, the cargo loader, the truck manufacturer, and even the maintenance contractor can all carry separate insurance policies. A thorough investigation by your attorney may reveal defendants beyond the obvious ones.

-

Preserve electronic evidence immediately. Event data recorders, also called black boxes, and telematics systems record speed, braking, hours of service, and GPS data. This data can be overwritten or destroyed within days. Your attorney can send a preservation letter within hours of taking your case.

-

Get your own independent medical evaluation. Insurers will send you to their preferred doctors. Getting an independent evaluation creates a second record of your injuries that cannot be dismissed as insurer-selected.

-

Understand the settlement timeline before you commit. Georgia’s statute of limitations for personal injury is two years, but complex trucking cases often take longer to resolve fully. Rushing a settlement to meet financial pressure is one of the most common mistakes victims make.

-

Work with a lawyer who specializes in trucking cases. General personal injury experience is not enough. Trucking claims involve FMCSA regulations, carrier maintenance records, driver qualification files, and multi-policy negotiations that require specific expertise.

Pro Tip: If the trucking company’s insurer contacts you in the days after a crash, you are not required to give a recorded statement. Politely decline and consult an attorney first.

Current coverage limits vs. what victims actually need

The disconnect between what the law requires and what serious injuries cost is the central problem in truck crash insurance reform. The numbers are stark, and they’re driving real legislative action.

Proposed 2026 legislation called the Fair Compensation for Truck Crash Victims Act would raise the federal minimum from $750,000 to $5 million and index future minimums to inflation. This would be the most significant update to trucking insurance requirements in decades, and advocates argue it is long overdue.

The case for reform is straightforward. A victim who suffers a spinal cord injury in a truck crash can face lifetime care costs well above $3 million. Under current minimums, the trucking company’s insurer may only be required to contribute $750,000 to that recovery. The rest falls on the victim’s own health insurance, government programs, or simply goes uncompensated.

There’s an additional dimension worth noting. Trucking fleets with strong safety cultures and technology investments consistently see lower insurance losses and premiums. That means the insurance system already rewards safer carriers. Raising minimums would add further incentive for companies to invest in safety, not just for legal compliance but for financial reasons.

For victims right now, before any legislation passes, the practical takeaway is this: the gap between minimum insurance requirements and real crash costs means you must treat your claim as a multi-policy, multi-defendant case from day one.

My perspective on insurance and truck crash victims

I’ve seen firsthand how victims walk into the claims process believing the insurance company will treat them fairly. That belief gets tested fast. What surprises most people isn’t that insurers push back. It’s how organized and methodical that pushback is.

In my experience, the cases that end in strong outcomes share one common trait. The victim or their family moved quickly to get legal representation before making any statements, signing any documents, or accepting any early offers. Every day that passes without legal counsel is a day the insurer’s team is working unchallenged.

What I’ve learned is that the minimum insurance discussion, while important for policy reform, can distract victims from the more useful question: what policies and defendants are actually available in my specific case? That answer almost always reveals more options than the victim initially knew existed.

The uncomfortable truth about truck crash insurance is that you can’t rely on the system to work for you automatically. You have to work it. That means knowing the questions to ask, preserving evidence, and refusing to settle until you fully understand what your injuries will cost over the rest of your life.

— Ali

How Jewkesfirm helps truck accident victims fight back

If you’ve been hurt in a truck crash, Jewkesfirm is ready to stand with you. The attorneys at Jewkesfirm understand the full complexity of trucking accident claims in Georgia, including how to identify every applicable insurance policy, challenge insurer tactics, and pursue the maximum compensation your case deserves.

Jewkesfirm offers FREE consultations with no obligation, and you pay nothing unless they win your case. Their team has recovered millions for injured clients across South Atlanta and surrounding Georgia counties. They know how insurance companies operate, and they know how to level the playing field on your behalf. Don’t face a trucking company’s insurer alone. Contact Jewkesfirm today and let a dedicated advocate fight for your recovery.

FAQ

What is the minimum insurance required for commercial trucks?

The FMCSA requires most interstate general freight carriers to carry at least $750,000 in liability insurance, though this minimum has not kept pace with inflation or modern medical costs and often falls short in catastrophic injury cases.

Can I pursue more than one insurer after a truck crash?

Yes. Many trucking companies carry excess and umbrella policies above their primary coverage, and multiple parties like the carrier, cargo loader, or maintenance company may each hold separate policies you can pursue.

What tactics do insurers use to minimize truck crash payouts?

Insurers commonly dispute liability, withhold key evidence like driver logs and black box data, and offer fast but low settlements before victims understand the full extent of their injuries.

Do I need a lawyer for truck accident insurance claims?

Working with an attorney experienced in trucking cases is strongly recommended. The claims process for truck collisions involves FMCSA regulations, multi-policy negotiations, and evidence preservation steps that are difficult to manage without legal expertise.

What is the Fair Compensation for Truck Crash Victims Act?

It is proposed 2026 federal legislation that would raise the trucking insurance minimum from $750,000 to $5 million and index it to inflation going forward, providing significantly stronger financial protection for crash victims.