TL;DR:

- Insurance adjusters determine claim payouts by investigating damages and negotiating settlements with a bias toward insurer interests. They are not neutral advocates, and their reports heavily influence claim outcomes. Proper documentation and understanding of adjuster tactics improve the chances of a fair settlement, especially in serious injury cases.

An insurance adjuster is a professional who determines how much an insurance company should pay on a claim by investigating losses, reviewing policy coverage, and negotiating settlements. In personal injury cases, the role of insurance adjusters is especially consequential. The adjuster’s findings directly shape whether your claim is approved, disputed, or reduced. Understanding what adjusters do, who they represent, and how to work with them gives you a real advantage when your health and finances are on the line.

What is the role of insurance adjusters in personal injury cases?

Insurance adjusters, also called claims adjusters, are the primary decision-makers in the claims process. Their core responsibilities include verifying policy coverage, inspecting accident scenes, interviewing involved parties, reviewing medical records, and negotiating final settlements. They manage every claim from the first notice of loss through to closure, ensuring compliance with both policy terms and applicable regulations.

One fact claimants often miss: adjusters are legally agents of the insurer, not neutral third parties. Their loyalty is to the insurance company, not to you. That does not make them adversaries, but it does mean their job is to resolve claims within the limits the insurer sets, not to maximize your payout.

Adjusters also coordinate with experts such as contractors, medical providers, and engineers to evaluate the full scope of a loss. In personal injury cases, this often means reviewing hospital records, consulting with medical professionals, and assessing long-term treatment costs. The adjuster’s report becomes the foundation for every settlement offer you receive.

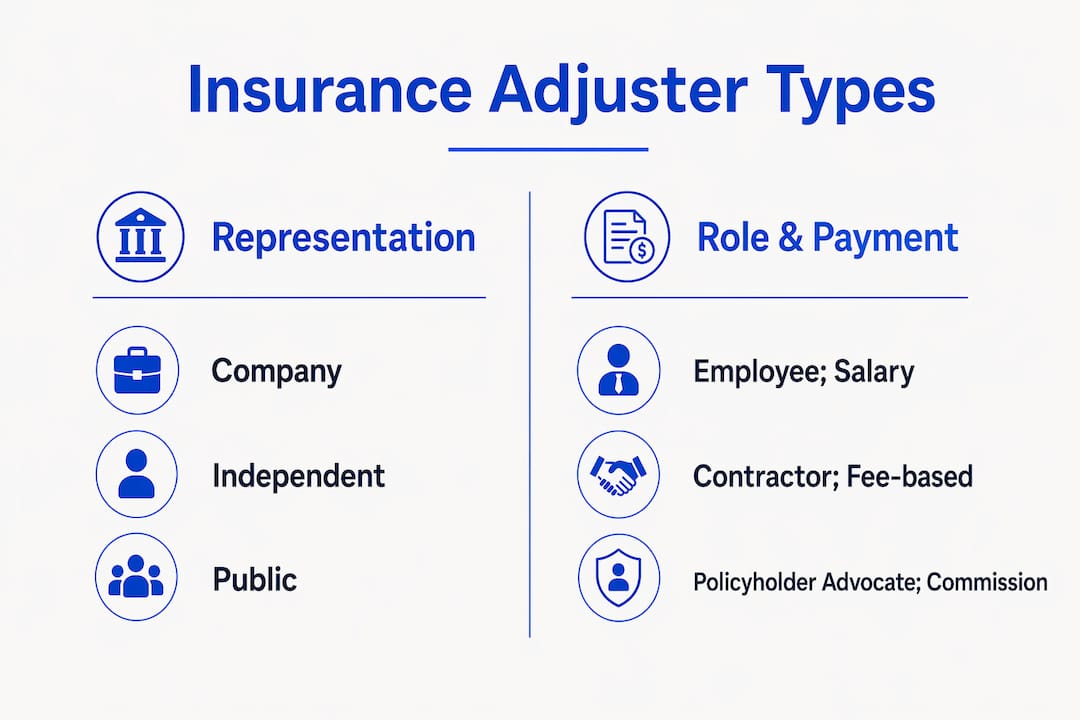

What are the different types of insurance adjusters?

Three distinct types of adjusters operate in the claims process, and each one serves a different principal. Knowing which type you are dealing with changes how you should approach every conversation.

| Adjuster Type | Who They Represent | How They Are Paid |

|---|---|---|

| Company (staff) adjuster | The insurance company | Salaried employee |

| Independent adjuster | The insurance company (on contract) | Per-claim fee |

| Public adjuster | The policyholder | 5–15% of settlement |

Company adjusters are salaried employees of the insurer. They handle routine claims and are trained to protect the company’s financial interests. Their goal is to settle claims accurately but efficiently, which often means keeping payouts within tight internal guidelines.

Independent adjusters work on contract for insurers, typically during high-volume periods or after large disasters. They are not insurer employees, but they still represent insurer interests. After major hurricanes or multi-vehicle accidents, insurers often deploy independent adjusters to manage overflow claims quickly.

Public adjusters are the only type who work directly for you, the policyholder. They advocate for the highest possible settlement and charge a percentage fee of 5–15% of the final payout for their services. That fee is worth considering carefully. On a $100,000 personal injury claim, a public adjuster’s fee could reach $15,000.

How do insurance adjusters investigate and evaluate claims?

The insurance claim adjusting process follows a structured sequence. Each step generates documentation that either supports or challenges your claim’s value.

- Verify coverage. The adjuster reviews your policy to confirm the loss is covered and identifies any exclusions or limits that apply. This step determines whether the claim moves forward at all.

- Inspect the scene or injuries. For personal injury cases, this means reviewing accident scene photos, police reports, and medical records. The adjuster may also conduct an independent medical examination through a physician of the insurer’s choosing.

- Interview all parties. The adjuster speaks with the claimant, witnesses, and sometimes the at-fault party. Everything said during these interviews is documented as evidence and can affect claim approval or dispute resolution.

- Review estimates and records. Medical bills, treatment plans, lost wage documentation, and repair estimates are all collected and analyzed. The adjuster may challenge estimates they consider excessive.

- Detect fraud. Insurance fraud is a felony in every U.S. state, and adjusters serve as the first line of defense. Special investigation units work alongside adjusters to flag inconsistencies in timelines, injuries, or damage reports.

- Document findings and set reserves. The adjuster prepares a written report and establishes a financial reserve for the claim. That reserve often exceeds the initial settlement offer, which is important to understand before you negotiate.

Pro Tip: Request a copy of the adjuster’s inspection report as early as possible. Their documented findings form the basis of every offer, and reviewing them lets you identify errors or omissions before negotiations begin.

What challenges do insurance adjusters face, and why does it matter to you?

Adjusters operate under real pressure, and that pressure directly affects how your claim is handled. Understanding their constraints helps you respond strategically rather than emotionally.

- Cost control vs. fair compensation. There is inherent tension between controlling insurer costs and fairly compensating claimants. Adjusters work within budgets and performance metrics that reward efficient claim closure, not maximum payouts.

- Workload spikes. Adjusters may work well over 40 hours during peak periods following disasters or large accidents. A backlogged adjuster may rush evaluations, which can result in undervalued claims.

- Authority limits. Adjusters operate within authority limits and require supervisor approval for significant claims. If your claim exceeds their authority threshold, expect delays and additional review layers before any offer is finalized.

- Emotional complexity. Adjusters handle disputes involving serious injuries and deaths. The professional detachment required to do that job can read as indifference to claimants who are in pain and under financial stress.

- Policy compliance vs. empathy. Adjusters must ensure claims comply with policy limits and exclusions. That obligation is sometimes mistaken for lack of empathy when it is actually a contractual requirement.

Pro Tip: If your claim stalls, ask directly whether it has exceeded the adjuster’s authority level. That one question can accelerate the process by prompting a supervisor review.

How can claimants work effectively with insurance adjusters?

Your behavior during the claims process has a direct impact on the outcome. The following practices protect your claim’s value from the first contact through final settlement.

- Document everything immediately. Photograph injuries, property damage, and the accident scene as soon as it is safe to do so. Learn why documenting accident scenes matters before you speak to any adjuster.

- Keep all records organized. Save every medical bill, treatment note, prescription receipt, and communication with the adjuster. Accurate documentation and clear communication consistently improve claim outcomes.

- Watch what you say. Do not speculate about fault, minimize your injuries, or make casual statements like “I’m fine.” Everything is documented. A single offhand comment can reduce your settlement significantly.

- Respond promptly but deliberately. Answer adjuster requests within a reasonable timeframe, but never rush a recorded statement without preparing first. You have the right to consult an attorney before giving any recorded interview.

- Understand the reserve. Adjusters maintain reserves for every claim, and those reserves often exceed the first offer. The first offer is rarely the final offer. Treat it as a starting point.

- Know when to get help. If your claim involves serious injuries, disputed liability, or a lowball offer, consider consulting a personal injury attorney or a public adjuster. Review the personal injury checklist for 2026 to confirm you have covered every step before accepting any settlement.

Understanding how insurance companies approach claims gives you additional context for why adjusters behave the way they do during negotiations.

Key takeaways

Insurance adjusters represent the insurer’s interests first, and your documentation, communication, and preparation determine how much leverage you have in every negotiation.

| Point | Details |

|---|---|

| Adjusters work for insurers | They are legally agents of the insurer, not neutral advocates for claimants. |

| Three adjuster types exist | Company, independent, and public adjusters each serve different principals with different incentives. |

| First offers are negotiable | Adjusters maintain reserves that often exceed initial settlement offers, leaving room to negotiate. |

| Documentation drives outcomes | Accurate records of injuries, expenses, and communications directly improve claim results. |

| Authority limits cause delays | Large claims require supervisor approval, so expect additional review layers on significant personal injury cases. |

What I have learned about dealing with insurance adjusters

The biggest mistake I see claimants make is treating the adjuster like a helpful neutral party. Adjusters are professionals doing a job, and that job is to resolve claims within the insurer’s financial interests. That is not cynicism. It is just the structure of the relationship.

What surprises most people is how much the adjuster’s documentation shapes the entire outcome. Their photos, measurements, and notes become the primary evidence in any dispute. If their report understates your injuries or misrepresents the accident scene, correcting that record later is an uphill battle. Your own documentation, gathered immediately after the accident, is the most powerful tool you have.

I have also seen claimants unknowingly damage their own claims in the first phone call. A casual “I’m doing okay” to an adjuster asking how you feel gets documented. Weeks later, when you are still in physical therapy, that comment becomes a contradiction the insurer uses to challenge your injury claim.

The practical lesson is this: prepare before every adjuster interaction, document before you speak, and never accept a first offer without understanding what the reserve looks like. When the claim involves serious injuries or disputed liability, experienced legal counsel levels the playing field in ways that documentation alone cannot.

— Ali

Protect your claim with dedicated legal support

Dealing with insurance adjusters after a personal injury is stressful, and the stakes are high. Jewkesfirm has recovered millions for accident victims across South Atlanta and surrounding Georgia counties, and their team knows exactly how insurers approach claims.

Jewkesfirm offers free consultations with no obligation, and you pay nothing unless they win your case. Their attorneys understand adjuster tactics, authority limits, and reserve strategies, and they use that knowledge to fight for the maximum compensation you deserve. If you have been injured and an adjuster is already involved, do not wait. Call Jewkesfirm today for a FREE CASE REVIEW and make sure your voice is heard.

FAQ

What does an insurance adjuster actually do?

An insurance adjuster investigates claims by verifying coverage, inspecting damages or injuries, interviewing parties, and negotiating settlements on behalf of the insurer. Their findings directly determine the value of your claim.

Are insurance adjusters on my side?

No. Company and independent adjusters are agents of the insurer and represent the insurance company’s interests. Only a public adjuster, who you hire and pay separately, advocates for your maximum payout.

Can I negotiate with an insurance adjuster?

Yes. The first settlement offer is rarely final. Adjusters maintain claim reserves that often exceed initial offers, so presenting strong documentation and a clear demand letter gives you real negotiating room.

When should I hire a personal injury attorney instead of a public adjuster?

Hire a personal injury attorney when liability is disputed, injuries are serious, or the insurer denies your claim. An attorney handles litigation and legal strategy, while a public adjuster focuses only on claim valuation. Review the auto accident victim checklist to assess which type of help fits your situation.

How long does the insurance claim adjusting process take?

Simple claims may close within a few weeks, but personal injury claims involving medical treatment, disputed liability, or large reserves can take several months. Adjuster workload spikes after disasters can extend timelines further.